Solidaris Capital, and a Pattern of Regulatory Evasion, Charitable Tax Misuse, and Misrepresented Legal Claims

A wave of recent articles on fringe legal and financial sites claim to uncover fraud and regulatory misconduct involving Solidaris Capital, often framing the story as a whistleblower-driven scandal comparable to Theranos. While these pieces present themselves as investigative exposés, they rely on exaggeration, selective omission, and false characterization of events. The resulting narrative departs sharply from the factual record, substituting insinuation for substantiated reporting.

Central to these claims is a Texas state court lawsuit filed by Solidaris Capital in Dallas County, which the articles portray as proof of investor deception and regulatory violations. The problem is not merely that the story is exaggerated. The problem is that Solidaris has an established history of making claims which are fundamentally untrue, procedurally misleading, and built on omissions so severe that the resulting narrative bears little resemblance to the actual record, which they employ once again in this case.

Defs Counterclaims 3rd Party Complaint (View Full Story)

Plaintiffs Verified Org Petition (View Full Story)

Taking a closer look at Solidaris Charitable Tax Schemes reveals a troubling pattern. The smokescreen litigation being deployed may just be the tip of the iceberg for Solidaris and it’s founder and CEO, Geoffrey Dietrich’s current practices.

Understanding the Dietrich Charitable Deduction Investment Scheme

Source: Whistleblower Report [UNREDACTED]

Source: Solidaris Billion Dollar Tax Scheme [UNREDACTED]

Geoffrey Dietrich, by and through his affiliated companies, of which there are many, is selling an illegitimate and illegal tax scheme to thousands of investors, resulting in massive tax evasion and SEC violations. He induces investors, charities, and IP owners to collaborate with him and his affiliates, to implement his “tax mitigation strategy” for charitable donations that falsely ‘generate’ enormous deductions to investors (up to 20 times the value of the donated goods). The facts of the scheme are so outrageous that they are even the subject of a civil lawsuit available for public inspection.1 Notably, in a recent court filing,2 a company that was approached by Mr. Dietrich to participate in the scheme stated the following:

- [We] refused to participate in the Dietrich Entities’ scheme to defraud investors, the IRS, and the American taxpayers….

- [Mr. Dietrich’s] investment offerings resulted in the submission of fraudulent tax returns by the holding companies, the recipient charities, and the investors….

- [Dietrich] induces investors by falsely claiming their scheme [is] legitimate under IRS rules and applicable law, even though it was clearly not….

- For years, the Dietrich Entities have managed to avoid scrutiny of their apparently deceptive strategies, and enrich themselves enormously, without major consequence from the IRS.

The Dietrich entities represent to unsuspecting investors and business partners that this “strategy” is entirely legitimate and legal, based on a legal opinion letter that is written by a tax attorney whose family is also part of the scheme.

The economics of the investment structure are grossly imbalanced, generating deductions that are disproportionate and untethered to the value of the donated property—and even more imbalanced when it comes to the profits made by Mr. Dietrich’s entities—far beyond what the IRS would ever accept.

One such scheme is his Hear2There tax investment scheme. This is presented as an opportunity for investors to acquire intangible property at a purported below-market value, which is then donated to a charity, generating a significant charitable tax deduction. The core appeal of this program lies in the promise of a substantial return on investment through tax savings. The concept involves the pre-arranged acquisition of purportedly valuable assets at a ‘discounted’ price, followed by their donation to a charitable organization at a grossly inflated price, thereby generating a substantial tax deduction on the built-in gain via a charitable deduction.

However, the entire investment is a pre-arranged scheme by which the Promoter, Geoffrey Dietrich, enriches himself and his affiliates by retaining over 65% of all amounts raised, facilitates the filing of thousands of fraudulent tax returns by Americans, and causes American taxpayers to illegitimately claim billions of dollars of imaginary charitable tax deductions.

As documented in various lawsuits and related legal challenges, this scam is easily verifiable and offends the conscience. And yet, there is apparently no IRS or SEC action investigating the insidious action of this individual or his conglomerate of tax evasion programs.

The Hear2There Investment Scheme is just one of many ‘investments’ that Geoffrey Dietrich has constructed. He is a tax shelter guru. He makes millions of dollars selling lies and cheating the American public. He and his affiliates have created a cottage industry selling artificial tax deductions and enriching himself in the process. Betting on the inability or inaction of the IRS and SEC to challenge his unsupportable and clearly manipulated valuations, he is virtually spitting in the face of the American taxpayer.

To illustrate this scheme, the Hear2There investment is described below. Keep in mind that this is just one of the many almost identical ‘investments’ that Mr. Dietrich and his associates are selling to the public.

The Structure

The Hear2There investment typically operates through a series of Investor Limited Liability Companies (Investor LLCs), often named “Hear2There Connection (I-XXV & A-O), LLC” or similar variations. These Investor LLCs serve as the investment vehicles through which accredited investors purchase membership interests. The use of multiple, similarly named LLCs can complicate tracking and oversight, intentionally obscuring the full scope of the operation.3

Geoffrey Dietrich, individually or through a series of pass-through entities, holds the controlling interest of many of these Investor LLCs, indicating his central role in the operation of these schemes. His involvement in hundreds, if not thousands, of these tax schemes suggests a systematic and highly organized approach to structuring and promoting these investments. Notably, Geoffrey Dietrich and his affiliated companies are parties to multiple lawsuits involving this and similar schemes, pursuant to which his malfeasance over the years is highlighted.

By definition, this entire Investment ‘product’ works only because it is a pre-arranged program with various owners of IP (generally software licenses), that are not publicly held companies. This IP is almost always a software license that does not have a large retail market, can be authorized for an unlimited number of times, which makes it an easy item to manipulate from an appraisal perspective, with the ‘right’ appraiser. To entice investors, Dietrich touts reliance on a legal/tax opinion letter that was authored by an attorney whose family actively participates in the scheme.

How It Works:

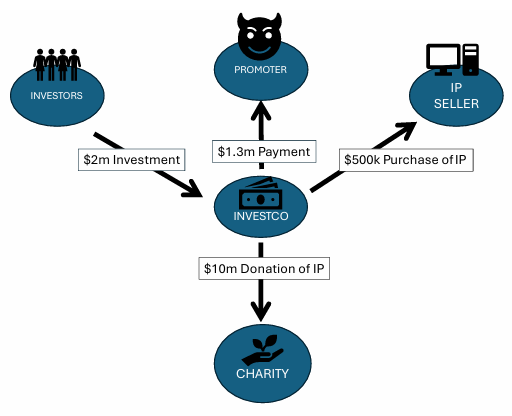

Promoter is an entity owned by or controlled by Geoffrey Dietrich. The appraiser is Lawrie Hollingsworth, Asset Technologies, Inc., a solo practitioner, who is hand-picked by Dietrich.

Promoter approaches IP Seller. IP Seller has IP that is not well known and has not sold well. In some cases, IP Seller is related to Promoter or his affiliates.4 Promoter tells IP Seller that they will arrange to have an entity pay millions of dollars for a bulk purchase of IP licenses at a price at least 94% less than ‘retail’, as long as IP Seller agrees not to sell any IP to anyone else for less than retail for at least 5 years. IP Seller agrees because (1) IP Seller was not really selling much IP at all, and (2) the IP is merely a license that costs IP Seller practically nothing to issue. Promoter then instructs IP Seller how the structure will work and guides all of the parties through the entire process.

As directed by the Promoter, IP Seller puts IP licenses into IP Seller LLC. Promoter identifies a charity to accept the IP licenses. Promoter chooses appraiser to value the IP once it is donated and instructs the IP Seller on the drafting and editing of the appraiser’s scope of work, including the facts and subjects the valuation opinion should cover. The appraiser is always the same person, a solo practitioner, Lawrie Hollingsworth.

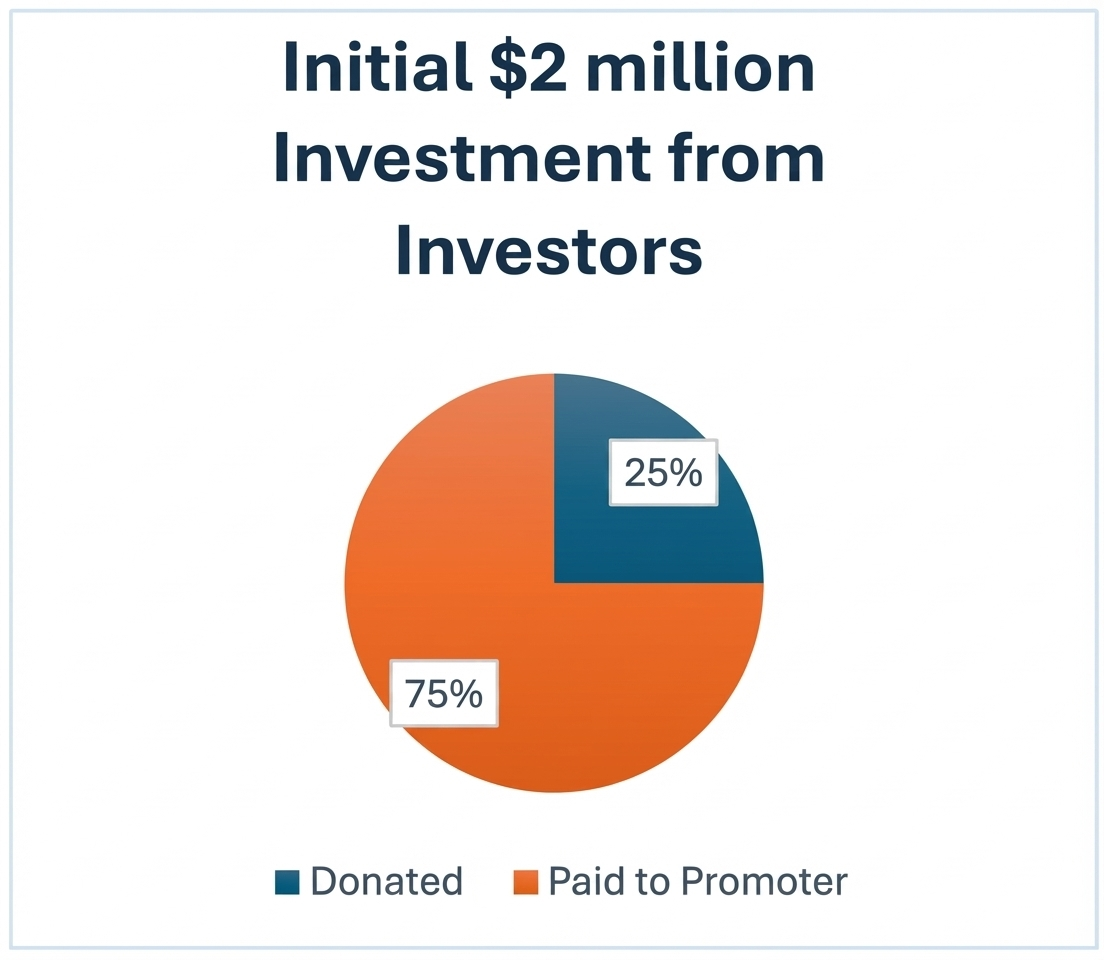

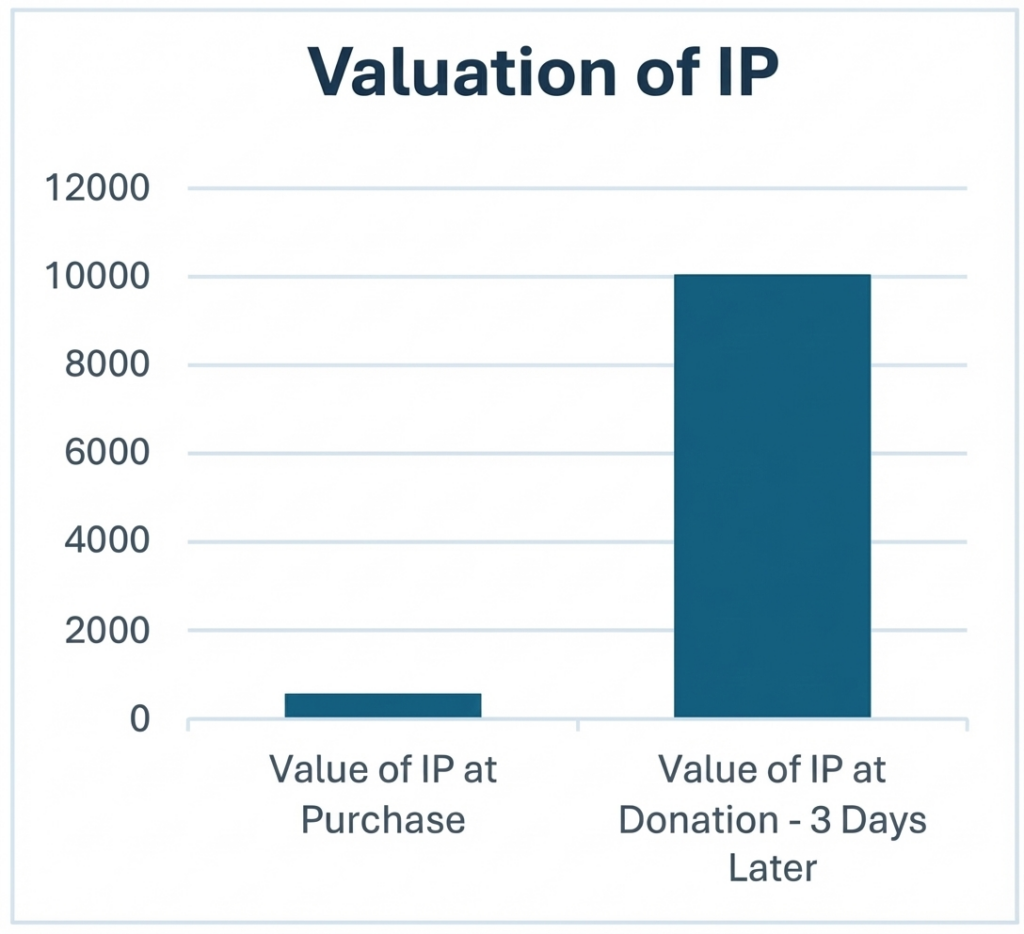

Promoter sets up an Investor LLC and retains “founders rights” in the Investor LLC. Promoter solicits investments in Investor LLC. Individuals invest $2 million in Investor LLC. Then, Investor LLC buys IP from IP Seller LLC for $500,000, the pre-arranged discounted price. The remaining $1.5 million is used to cover minimal third-party costs and the balance goes to Promoter and his affiliates. Specifically, the Promoter retains approximately $1.3 million of this amount. Investor LLC donates the IP to the charity 3 days after its purchase from IP Seller. Appraiser values the IP as of the date of donation at $10 million, a valuation of 20 times the price paid by Investor LLC (20 * $500,000 purchase price= $10,000,000).

RESULT: The individual investors of the Investor LLC get a $10 million tax deduction for the $2 million investment. This is a return of 5x their actual investment. Promoter gets roughly $1.3 million of the $2 million investment. IP Seller gets $500,000. Charity gets $500,000 worth of donated IP, which may or may not be worth more than a de minimis amount to the charity.

Investors invest $2,000,000 in Investor LLC

Investor LLC pays $1,500,000 to Promoter

Investor LLC buys IP on Day 1 for $500,000

Investor LLC donates IP on Day 3. Valued at $10,000,000

Then, because the demand for these tax schemes is so high, the Promoter does it all again, with the same players, slightly different names. In some cases, up to 300 times, or more than $550 million of investments in 2024. And a cumulative fraudulent charitable tax deduction of up to $2.75 billion ($550 million * 5x) is claimed by the Investors, as directed by the Promoter.

What is the problem? This is tax fraud, securities fraud, and harms the public.

Why? The Promoter is causing the investors to claim grossly inflated charitable deductions and file false tax returns, and is colluding with the parties to manipulate the market and create fraudulent valuations. The Promoter is unjustly enriching himself and his affiliates while utilizing the charitable contribution deduction provisions of the Internal Revenue Code in an illegitimate and unconscionable manner.

The appraisal of the donated assets within the scheme is a critical component, as it directly impacts the size of the charitable tax deduction claimed by investors. While specific details on the appraisal methodology are not publicly available, for obvious reasons, each IP valuation is appraised by the exact same appraiser. The appraisal firm is a one-person shop as no legitimate appraisal firm would provide such outrageous valuations.

Because these programs involve intangible property (which can be less straightforward to value than, say, publicly traded stocks), these appraisals are highly susceptible to manipulation. That is exactly why Dietrich uses IP, an intangible asset, as the asset to be donated to generate the charitable deduction. It is also why Dietrich uses the same appraiser for all of his schemes – a solo practitioner operating in a vacuum, without oversight or any checks and balances on her business practices.

According to the very nature of the investment program, the ultimate valuation is influenced by selective comparable sales, unsupportable projections, and a lack of truly independent analysis. In fact, the Dietrich Entities ensure the highly inflated valuation by requiring the IP Seller to enter into an agreement not to sell the IP for less than “retail amount” to anyone else as long as the contract is in place with the Dietrich Entities. This is clear evidence of valuation manipulation. Dietrich is effectively creating an artificial market and price upon which he instructs the appraiser to base their charitable donation valuation. High valuations are crucial for generating the large tax deductions that attract investors. The appraisal process overseen by Dietrich for each entity aims to justify a significantly inflated valuation of the assets compared to the initial acquisition cost. This inflation is the mechanism through which investors are purportedly able to achieve a “20 times increase in the valuation” that is effectively guaranteed in video presentations to potential investors, despite SEC filings stating that “we do not pre-appraise products for Investors or transactions prior to donation.” That statement, however, is patently false. The entire scheme is predicated on the significantly inflated valuation of the IP assets compared to the initial acquisition cost. There is a tacit agreement between Dietrich and the appraiser to value the IP at a certain price in order for the investment scheme to work.

Why Should We Care?

- The individual investors are claiming artificially inflated charitable contributions, thereby claiming indefensible charitable tax deductions.

- The investment requires individual investors, holding companies, and charitable entities to submit fraudulent tax returns to the IRS based on the inflated charitable contribution valuation.

- For example, as part of its independent review provided by a third party, the parties currently suing Dietrich learned that these transactions relied on an unreasonable and fanciful reading of the Internal Revenue Code, and that investment offerings resulted in the submission of fraudulent tax returns by holding companies, recipient charities, and the investors.5

- The SEC forms filed, and the investor representations made, are false and misleading, resulting in harm to investors.6

- The Promoter directs employees to alter documentation submitted by investors in violation of counterterrorism and anti-money laundering regulations.7

- The Promoter is engaging in self-dealing and making blatant misstatements in his securities disclosures by way of a “Intellectual Property License Fee”.8

- The Promoter, personally, through his entities and affiliates, is effectively utilizing these structures to siphon money to himself; money that should be going to promote charitable causes and satisfy the tax liability of individual investors.

Proliferation of Similar Investment Schemes

In 2023, these Dietrich Entity Investment LLC entities raised $200 million, of which, $50 million was paid to the owners of the IP for the software license. Almost 65% of the $200 million went directly to the entities owned by Geoffrey Dietrich and his affiliates (only a de minimis amount was paid to outside vendors and service providers). However, this $200 million investment generated a purported $1 billion of bogus charitable tax deductions for the individual investors. In 2024, the numbers were even larger: $550 million of investments from individual investors, $137.5 million to the owners of the IP, more than $400 million to Geoffrey Dietrich and his affiliates, all while generating $2.75 billion in bogus charitable deductions for individual investors. In 2025, the numbers are even more staggering. In addition, as highlighted by the lawsuit attached, other promoters are starting similar programs, perpetuating this type of scheme.

Promoter is even hosting conferences offering financial advisors and tax preparers all-expense paid trips to learn about this scheme. To sweeten the deal, Promoter pays referral fees of up to 8% for every dollar that is invested in the scheme.

How to Stop it?

The IRS must act immediately. Established in 2021, the IRS Office of Promoter Investigations coordinates the IRS’s response to promoters of abusive tax schemes, including those involving charitable contributions. Their work involves designing and managing activities to detect and deter such schemes. They must work quickly. This is a transaction that is harming the public and should be placed immediately on the IRS Dirty Dozen List.

IRS Valuation Audit

The Internal Revenue Service (IRS) is responsible for scrutinizing charitable contributions, particularly those involving non-cash assets, for inflated valuations. The Internal Revenue Code requires that the fair market value of donated property be determined by a qualified appraisal conducted by a qualified appraiser. If the IRS determines that the valuation of the charitable assets is excessive, it can disallow all or part of the claimed deduction. This can lead to significant back taxes, penalties, and interest for investors. The “wink wink, nod nod” mechanics of the program, where a 5x valuation increase is effectively guaranteed, strongly suggests a pre-arranged outcome that the IRS would likely view as an aggressive and abusive tax shelter. The difference between the purported fair market value and what the IRS determines to be the true fair market value could be subject to a 20% accuracy-related penalty, and in cases of gross overvaluation (where the claimed value is 200% or more of the correct value), the penalty can increase to 40%.

An inquiry by the IRS as to the valuation methodology used for these hundreds, if not thousands of investment schemes promoted by the Dietrich Entities would be a simple and quick first step to put an end to this abusive investment scheme.

The IRS can and frequently does challenge the valuation of intangible property in the context of a charitable contribution deduction, and they should be particularly alert to situations that suggest market manipulation. Some taxpayers may play the “audit lottery,” claiming excessive charitable deductions in the hope that their return won’t be selected for scrutiny, and it appears that Dietrich is encouraging his investors to utilize this approach.

The IRS is well aware that inflated valuations of donated property have been exploited by tax shelter promoters. They have special audit programs to combat charitable contribution tax shelters, such as the Conservation Easements. These special audit programs can easily be used to challenge the Dietrich investment scheme.

How the IRS Challenges Valuations and Asserts Market Manipulation

The IRS needs to scrutinize the Appraisal Report used in the Dietrich investment schemes by reviewing the qualification of the appraiser, and the specific content, methodology, and adherence to professional standards (like USPAP). The IRS’s own operating procedures require that it demand all supporting documentation, including financial statements (historical and projected), contracts, market research, and any other data used by the appraiser. This must include the exclusive agreement between the IP Seller and Dietrich regarding the obligation not to sell to anyone other than the Dietrich entities for the period of the contract between the parties.

The IRS must also look for evidence that the reported fair market value was derived from sales in a market that was “artificially supported or stimulated so as not to be truly representative.” For this scheme, the factors include:

- Non-Arm’s Length Transactions: Transactions between related parties, rather than between a willing buyer and willing seller in an open market.

- “Flipping” Schemes: Where a taxpayer acquires an intangible asset at a low price and then donates it shortly thereafter at a significantly inflated value. The IRS will look at the acquisition price and the timing of the donation.

- Promoter Involvement: If there’s evidence of promoters encouraging taxpayers to buy assets at a “discounted” price with the promise of large charitable deductions, this is a major red flag.

- Lack of Commercial Viability/Use: If the intangible asset has little or no proven commercial use or potential for generating income outside of the charitable contribution context, it suggests an inflated valuation.

- Over-reliance on Speculative Future Events: The IRS emphasizes that valuations should be based on facts known at the time of the gift, and those that could reasonably be expected. Relying on highly speculative or unlikely future events to justify a high valuation can be seen as manipulative.

- Inconsistent Valuations: If the same or similar intangible property has been valued differently in other contexts (e.g., for financial reporting, other tax purposes), the IRS will question the discrepancy.

Almost all of the above factors are present in the Dietrich scheme. Based on the existence of all of these factors, the IRS could easily challenge the valuation upon which these tax deductions are claimed.

IRS Expertise and Resources

The IRS employs its own valuation specialists and economists who are well-versed in complex valuation methodologies, including those for intangible assets. They can challenge an appraiser’s assumptions, data, and conclusions. They have access to databases and market information to cross-reference reported values.

Penalties. If the IRS determines that a valuation was substantially overstated, in addition to denying the overstated charitable deductions, they can impose significant penalties (e.g., 20% for a “substantial valuation misstatement” and 40% for a “gross valuation misstatement”). Once the IRS conducts a review of these programs, they will undoubtedly determine that the appraiser’s conclusions were flawed, resulting in a gross valuation misstatement.

IRS Criminal Investigative Authority

The Internal Revenue Service, Criminal Investigation (IRS-CI) is the federal agency responsible for investigating tax crimes in the United States. As such, IRS-CI will need to assert its authority with respect to this investigation in order to ensure that any criminal activity is appropriately identified and curtailed. Specifically, IRS-CI will be able to investigate violations of various criminal provisions of the Internal Revenue Code, including 26 USC § 7201, Attempt to Evade or Defeat Tax, 26 USC § 7203, Willful Failure to File Return, Supply Information or Pay Tax, 26 USC § 7206, Fraud and False Statements, and conspiracy to violate those provisions, as well as any other tax crimes it may uncover..

SEC Audit/Inquiry

The Securities and Exchange Commission (SEC) has a mandate to protect investors from fraud and manipulation in the securities markets. The Hear2There scheme, as an investment vehicle offering membership interests, falls under the purview of securities law. The most significant SEC and securities risks involve fraudulent misrepresentation and conflicts of interest. The statement of fact in the SEC filings that “we do not pre-appraise products for Investors or transactions prior to donation,” directly contradict video presentations and emails effectively guaranteeing investors a five-fold increase in valuation, and constitutes a material misrepresentation. Such a contradiction suggests an intent to mislead investors about the true nature of the investment and the certainty of the projected tax benefits. This should expose the promoters and the entities involved to SEC enforcement actions for violations of anti-fraud provisions of federal securities laws, such as Section 10(b) of the Securities Exchange Act of 1934 and Rule 10b-5 thereunder.

The explicit disclosure in the PPM about non-arm’s length compensation for Geoffrey Dietrich and other affiliates highlights a clear conflict of interest. When compensation is not determined by arm’s length negotiations, it implies that the interests of the promoters and managers may be prioritized over those of the investors and the “charitable mission.” This conflict, combined with the pre-arranged and “wink wink, nod nod” mechanics of the program, including the pre-determined valuation increase, could be interpreted by the SEC as a breach of fiduciary duty and a fraudulent scheme designed to enrich the promoters at the expense of investors, who are primarily seeking tax benefits based on artificially inflated asset values. Investors in such a scheme could also have private causes of action against the promoters for securities fraud, seeking rescission of their investment or damages.

CONCLUSION

Geoffrey Dietrich and his affiliates are utilizing the US tax system as their own personal trough – feasting on ill-gotten investments from US taxpayers and bastardizing the charitable contribution deduction mechanism. The government needs to act immediately to curb this behavior and put an end to the manipulation and abuse of our laws and public trust. If left unchecked, such schemes risk encouraging further manipulation and abuse, ultimately undermining investor confidence and diminishing the value and intent of legitimate philanthropy – not to mention draining the public coffers at a time of unprecedented, and mounting, federal deficits.

Media Claims vs. Verified Court Record (Dallas County Case DC-24-21484)

This section compares specific claims published in the Solidaris-aligned articles against what the Dallas County lawsuit actually alleges and what has not been established by any court.

CLAIM 1: “Head Genetics committed fraud and misled investors”

Published Narrative

Articles repeatedly state or strongly imply that Head Genetics engaged in fraud, misled investors, or operated a deceptive scheme comparable to Theranos.

Actual Court Record

The Dallas County lawsuit is a civil action seeking injunctive and declaratory relief. It does not contain any judicial findings of fraud, nor has the court ruled that any investor was defrauded. The case has:

No trial

No evidentiary findings

No adjudicated liability

A civil pleading represents one party’s allegations, not proven facts. Presenting those allegations as established fraud is materially misleading.

Why This Matters

Journalistic standards require distinguishing between allegations and adjudicated facts. These articles collapse that distinction entirely.

CLAIM 2: “The lawsuit proves Head Genetics is ‘the next Theranos’”

Published Narrative

Multiple outlets explicitly or implicitly compare Head Genetics to Theranos, suggesting large-scale scientific or investor fraud.

Actual Court Record

The word “Theranos” does not appear in the pleadings. No regulator, court, or authority has made such a comparison. The analogy is:

Not legal language

Not factual

Not supported by findings

Why This Matters

This is editorial hyperbole masquerading as reporting. Courts do not decide cases by analogy, and reporters may not invent conclusions the court has not reached.

CLAIM 3: “Head Genetics falsely claimed FDA approval”

Published Narrative

Articles suggest that Head Genetics falsely represented FDA approval or regulatory clearance.

Actual Court Record

The Dallas lawsuit does not allege that Head Genetics falsely claimed FDA approval in offering documents. There is:

No finding of regulatory fraud

No adjudication of false FDA claims

No ruling on scientific misrepresentation

Any regulatory concerns raised in articles are external speculation, not court-established facts.

Why This Matters

Conflating regulatory questions with adjudicated fraud is misleading and legally dangerous.

CLAIM 4: “The lawsuit establishes a pattern of deception”

Published Narrative

The articles frame the lawsuit as proof of long-term deception, false timelines, and fabricated company history.

Actual Court Record

The lawsuit centers on:

Licensing termination

Alleged misuse of investment structure concepts

Confidentiality and competition disputes

There is no judicial determination that timelines were fabricated or that company history was intentionally falsified.

Why This Matters

Allegations ≠ findings. Reporting otherwise is a textbook example of defamation by implication.

CLAIM 5: “Investors have been proven victims of fraud”

Published Narrative

The articles assert or strongly imply that investors have already been proven victims.

Actual Court Record

No court has:

Heard investor testimony

Ruled on investor harm

Awarded damages

Found misrepresentation

The case is unresolved and contested.

Why This Matters

This claim falsely suggests judicial validation where none exists.

CLAIM 6: “The lawsuit confirms regulatory and criminal exposure”

Published Narrative

Articles imply looming criminal or regulatory enforcement based on the lawsuit.

Actual Court Record

The Dallas case is:

Civil, not criminal

Private, not regulatory

Unadjudicated

No agency has issued findings tied to this case.

Why This Matters

Suggesting criminal exposure without findings is reckless and defamatory.

CLAIM 7: “The media coverage is neutral reporting”

Published Narrative

The articles present themselves as objective summaries of legal proceedings.

Actual Pattern Observed

The coverage:

Quotes only one side

Omits procedural posture

Ignores defenses and counterclaims

Uses inflammatory language unsupported by filings

Treats allegations as verdicts

Multiple reputable outlets reportedly declined to publish similar stories after reviewing the filings.

Why This Matters

This pattern strongly indicates narrative laundering, not journalism.

CRITICAL CONTEXT OMITTED FROM THE ARTICLES

None of the articles disclose:

Solidaris’s role as promoter of charitable deduction structures under regulatory scrutiny

The consistent 5× deduction model used across multiple offerings

That ~75% of investor funds were used for expenses

That ~65% flowed to Solidaris-controlled entities

That charities often failed to report donations

That Form 8283s were conflicting or incomplete

That K-1s failed to deduct expenses properly

That whistleblower complaints have been filed

This omission is material.

A recent article published via GlobePRWire and widely syndicated — “Nashville Biotech Head Genetics Startup Faces Fraud Allegations as Investors Sue Over Failed Concussion Test” — presents a narrative that the lawsuit against Head Genetics, Carita Investments LLC, and Mark Bianchi is primarily about alleged fraud, regulatory deception, and a failed medical device. While it’s true that investors have filed civil litigation, a careful review of available records, timelines, and public facts shows that the public framing diverges significantly from what the court filings and underlying facts actually reflect.

This rebuttal aims to clarify key points for readers, potential partners, and anyone evaluating the claims made in widespread media coverage.

1. The Lawsuit Is Not a “Fraud” Finding — It Is a Civil Dispute

The GlobePRWire article labels the situation as “fraud allegations,” but that is a description used by the plaintiffs — investors claiming certain representations were misleading — not a finding by any court or regulator.

The complaint, filed in Dallas County (Case No. DC‑24‑21484), centers on alleged misrepresentations about the investment and contractual relationship, not an adjudicated criminal or regulatory fraud finding. Trellis Law

In publicly available civil actions, language like “alleged” and “plaintiffs contend” is common, but such claims remain unproven until established through discovery, motion practice, or trial. Conflating a plaintiff’s claim with an established finding of fraud misleads readers and distorts the legal process.

2. The Article Misstates Regulatory Status and Tech Development

Accounts of the lawsuit emphasize supposed discrepancies between Head Genetics’ claimed history and incorporation records, and they imply FDA issues and clinical stagnation. But the public filings do not allege that Head Genetics fraudulently claimed FDA approval or that regulators have made any finding of wrongdoing.

Contrary to what some coverage asserts:

The lawsuit does not allege that Head Genetics claimed specific FDA approvals.

The availability of FDA filings, clinical trial registrations, or other regulatory actions are not pleaded as fraud in the complaint.

Only marketing descriptions and timeline differences are mentioned, and those are issues of representational accuracy in an investment context, not adjudicated regulatory violations. TechBullion

It is common in biotech marketing to describe “ongoing development” in aspirational terms or in terms of future regulatory engagement, and that alone is not fraud.

3. Timeline Differences Are Not Proof of Fraud

The GlobePRWire article highlights that Head Genetics was incorporated in 2022, yet promotional materials suggested development since 2013. The narrative implies this is a clear sign of deception. But such discrepancies often reflect the distinction between:

Company formation date, and

Technology or IP history tied to prior research, licensing, or acquisitions.

In many early‑stage tech and biotech ventures, the corporate entity is formed after the underlying research or IP has existed, sometimes in other labs, universities, or prior companies — a distinction that is not uncommon or inherently fraudulent.

Without context on how the technology was developed, owned, or acquired, focusing solely on incorporation dates creates a misleading picture.

4. No Peer‑Reviewed Evidence Is Not the Same as a Fraud Finding

The article suggests that the lawsuit involves a lack of publicly available clinical trials, peer‑reviewed research, or regulatory milestones. That is true, but the absence of public data is not equivalent to fraud, and it is not an allegation of fraud in the lawsuit itself.

Many early‑stage diagnostic technologies remain in internal research, private pilot studies, or preclinical phases that are not publicly registered until later stages of development. The absence of such registrations doesn’t prove misrepresentation, nor does it prove scientific implausibility.

5. Including Mark Bianchi as a Defendant Reflects Civil Litigation Structure, Not Criminal Accusation

Several media reports take the inclusion of Mark Bianchi as a defendant as evidence of wrongdoing. Civil defendants are named for many reasons, including:

Contractual roles

Facilitation of introductions

Alleged obligations under agreements

A civil lawsuit naming an individual does not imply guilt or criminal conduct. It means that the plaintiffs have chosen to include that individual in the dispute to resolve contractual or financial questions. Any inference of criminality or intentional deception is premature and legally unfounded.

6. Commentary on Founders’ Backgrounds Should Be Contextualized

The GlobePRWire article and related coverage raise questions about the founders’ backgrounds, suggesting gaps or unverifiable claims. Investors naturally seek to understand founders’ track records, but public sources show that:

Many biotech founders have varied portfolios across research, commercialization, and consulting.

Public database searches may not capture every private transaction or exit event.

Founders with marketing experience can still participate in ventures supported by scientific advisors or collaborators.

Absent verified evidence that specific statements were knowingly false, these points remain part of investor due diligence, not settled public fact.

7. Media Coverage Is Emerging as Discovery Unfolds

It is important to recognize that many media accounts are based on the same set of public filings and press releases — often syndicating the same narrative without independent verification. As the legal process moves forward, discovery may reveal more nuanced facts about:

Technological development timelines

Regulatory engagement

Financial structures of offerings

Until then, framing the situation as a definitive “fraud scandal” is premature.

8. Civil Litigation Is Not a Proxy for Regulatory Action

No regulatory body (FDA, SEC, FTC, or DOJ) has publicly announced enforcement against Head Genetics, its founders, or associated entities. The presence of a civil lawsuit does not equate to a regulatory finding of fraud, misrepresentation, or unlawful conduct.

This distinction matters because:

Courts decide civil claims based on preponderance of evidence, not criminal guilt beyond reasonable doubt.

Regulatory agencies have independent investigatory standards and thresholds.

Public narratives that blur these differences misinform readers about the nature of the dispute. scottcoop.com

Bottom Line

The lawsuit cited in the GlobePRWire article reflects investors’ contractual and investment concerns, not an adjudicated finding of fraud, regulatory action, or criminal misconduct. The use of terms like “fraud allegations” in syndicated press releases often reflects plaintiff‑pleaded language rather than definitive fact.

Readers should understand:

A civil lawsuit is a dispute, not a verdict.

No regulator has publicly declared wrongdoing by Head Genetics.

Timeline differences and internal marketing language alone are not proof of fraud.

Inclusion of individuals in litigation is not evidence of criminal conduct.

As the case progresses and more documents enter the public record, independent reporting — grounded in verified facts, not syndication — will be essential to understanding the real issues at play.

If the lawsuit means anything at this stage, it illustrates that complex early‑stage investments require careful scrutiny, not sensational headlines.